Let me tell you something embarrassing.

When I got my first UK salary, I looked at the number at the bottom, felt something between confusion and grief, and closed the app.

I did not read a single line above it.

I just accepted it. Moved on. Told myself this is just how it works here.

Then I found out I had been taxed on every single pound I earned because my tax code was wrong. HMRC refunded me nearly £600.

Six hundred pounds. Sitting there. Mine. That I almost walked away from because I never read my payslip properly.

So this is the blog I wish someone had handed me on my first day of work in the UK. No jargon. No assumptions. Just a clear, honest walk through every section of your payslip and what it is actually telling you.

First — Where Do You Find Your Payslip?

Your employer is legally required to give you a payslip on or before every payday.

Most employers in the UK now issue payslips digitally through a payroll portal or by email. Some still issue paper ones. Either way, you are entitled to it and if you are not receiving one, that is a legal issue worth flagging to your HR department immediately.

The Sections Of A UK Payslip

Every payslip looks slightly different depending on your employer. But they all contain the same core information. Here is what to look for.

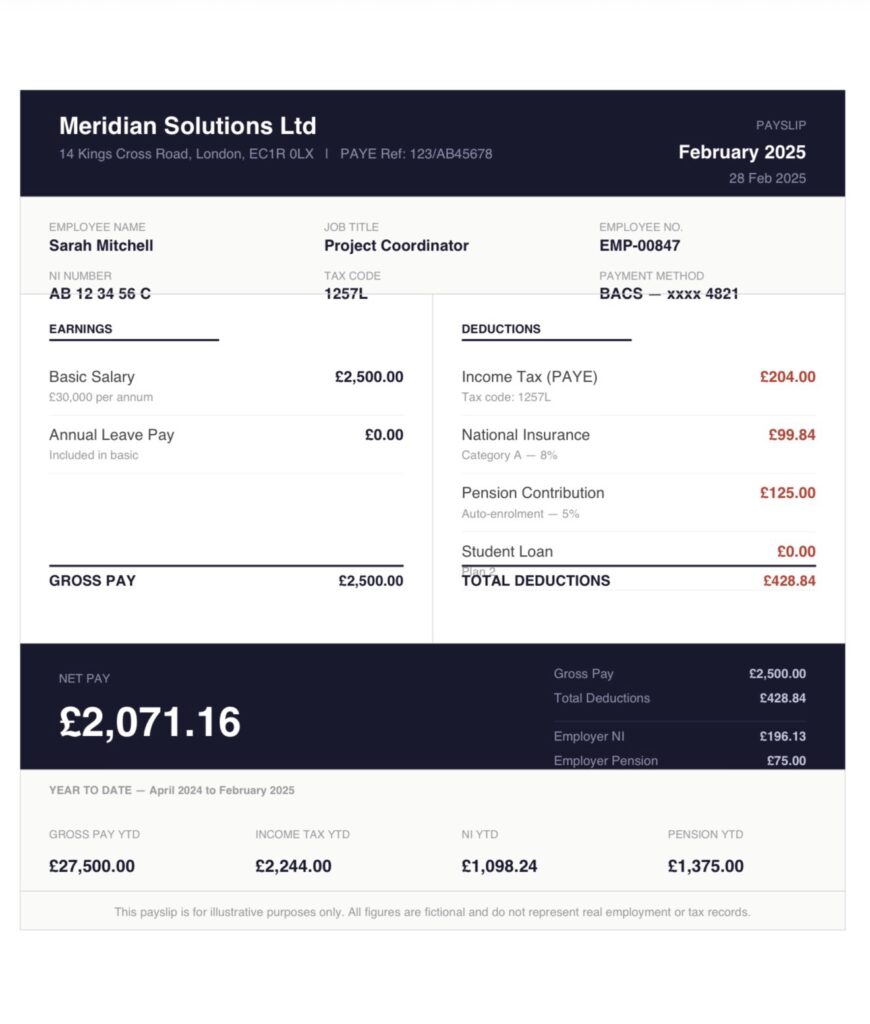

1. Your Personal Details

At the top of your payslip you will usually see your name, employee number, job title, NI number and tax reference.

Your NI number — National Insurance number — is yours for life. It follows you from job to job. Check that it is correct on every payslip. If it is wrong, flag it to payroll immediately.

Your tax reference is your employer’s PAYE reference with HMRC. You will need this if you ever have to call HMRC about your tax.

2. Your Tax Code — This Is The Most Important Thing On Your Payslip

I am going to say this clearly because most people skip straight past it.

Your tax code determines how much income tax is deducted from your pay. If it is wrong, you will either overpay or underpay tax every single month.

If you have one job, your tax code should be 1257L.

That number — 1257 — represents your Personal Allowance of £12,570. That is the amount you can earn in a full tax year completely tax free. HMRC does not touch it. The L at the end confirms your standard allowance is applied.

Common tax codes and what they mean:

1257L — Correct for most people with one job. Standard personal allowance applied.

OT — Emergency code. Zero personal allowance. You are being taxed on every single pound you earn from the first penny. This often happens when you start a new job and your employer does not yet have your tax details. If you see this, call HMRC immediately.

BR — Basic rate. Everything taxed at 20% with no personal allowance. Usually applied to a second job or pension but if it is on your main job something is wrong.

W1 or M1 — These appear after your main code and mean your tax is being calculated on a week by week or month by month basis rather than cumulatively across the year. This can happen when you start mid-year. It is not always wrong but it can sometimes mean you overpay and get a refund at year end.

1072L or similar reduced numbers — Your personal allowance has been reduced. HMRC does this if they think you have untaxed income elsewhere or if you owe tax from a previous year. If you do not know why your allowance is reduced, call HMRC and ask.

If your tax code is anything other than 1257L and you have one job with no unusual circumstances — call HMRC on 0300 200 3300 and query it. That call could be worth hundreds of pounds.

3. The Pay Period

This tells you which dates your payslip covers.

Some payslips show a week number — Week 1, Week 39 — which refers to the UK tax year that runs from April to April. Week 1 is the first week of April. Week 52 is the last week of March.

Some show calendar dates. Either way, check it matches the period you actually worked.

4. Gross Pay

This is your pay before any deductions.

If you are on a salary of £30,000 a year, your monthly gross pay is £2,500. That is the number your employer agreed to pay you in your contract.

Everything that follows is what comes out of that gross figure before the money reaches your account.

5. Income Tax — PAYE

PAYE stands for Pay As You Earn. It is the income tax your employer deducts directly from your pay before you receive it.

Here is how UK income tax works in simple terms for England, Wales and Northern Ireland:

Your first £12,570 — tax free. This is your Personal Allowance.

£12,571 to £50,270 — taxed at 20%. This is the basic rate band and is where most people in the UK sit.

£50,271 to £100,000 — taxed at 40%. This is the higher rate band.

£100,001 to £125,140 — this is where it gets brutal. HMRC starts removing your Personal Allowance — £1 for every £2 you earn above £100,000. By the time you reach £125,140 your entire Personal Allowance is gone. The effective tax rate in this band is 60%. Most people earning here have no idea that band exists.

Above £125,140 — taxed at 45% with no Personal Allowance.

Important — if you are in Scotland, your tax bands are different. Scotland has six bands with rates running from 19% to 48%. Check the Scottish Government website for your specific rates.

Your PAYE deduction on your payslip should reflect whichever band your income falls in. If it looks dramatically higher than expected, check your tax code first.

6. National Insurance

National Insurance is separate from income tax but it comes out of the same payslip — which is why your take home always feels lower than you expected.

A lot of people assume it is the same as income tax. It is not. It is a separate contribution that funds state benefits including the NHS, state pension and certain welfare payments.

As an employee you currently pay:

8% on earnings between £12,570 and £50,270 per year.

2% on everything above that.

So on a £30,000 salary, your monthly NI contribution is roughly £99 to £100.

Your payslip will also sometimes show your NI category — most employees are Category A which is the standard rate.

7. Pension Contributions

If you are employed in the UK and you are over 22 and earning above £10,000 a year, your employer is legally required to automatically enrol you into a workplace pension.

Your payslip will show your pension contribution — usually labelled as PenAutoEEs or Pension or the name of your pension provider.

The minimum employee contribution is currently 5% of your qualifying earnings. Your employer must contribute at least 3% on top of that.

I know it is tempting to opt out when money is tight. Please do not do it lightly.

Your employer’s contribution is free money going into your future. If you opt out, you lose their contribution too. At a £30,000 salary, your employer is adding £75 a month to your pension on top of your own £125. That is £900 a year from your employer alone — before investment growth.

8. Student Loan Repayments

Not everyone has a student loan deduction. But if you studied in the UK and took out a student loan, your repayments are collected through your payslip once your income crosses a certain threshold.

The threshold depends on which repayment plan you are on:

Plan 1 — you repay 9% on earnings above £24,990 per year.

Plan 2 — you repay 9% on earnings above £27,295 per year.

Plan 5 — you repay 9% on earnings above £25,000 per year.

Postgraduate Loan — you repay 6% on earnings above £21,000 per year.

If you are being charged student loan repayments and you are earning below your plan’s threshold — flag it to payroll immediately.

9. Net Pay

This is the number at the bottom. The one that actually lands in your account.

Gross pay minus all deductions equals net pay. That is it.

If this number ever looks dramatically lower than you expected, do not just accept it. Go back through every deduction line and check them against what you know about your tax code, your salary and your circumstances.

10. Year To Date Figures

This section appears on most payslips and most people ignore it completely.

YTD means Year to Date. It shows you the running total of all your earnings and deductions from the start of the UK tax year — which runs from 6 April to 5 April the following year.

So if you are looking at a February payslip, your YTD figures show everything accumulated from April to February.

Why does this matter?

Because at the end of the tax year HMRC reconciles everything. If your YTD income tax paid is higher than what you actually owed across the whole year, you are due a refund. If it is lower, you may owe the difference.

Keeping an eye on your YTD figures means you are never surprised when the tax year ends.

11. Holiday Remaining

Some payslips include a section showing how many days of annual leave you have left and when your holiday anniversary date falls.

In the UK you are legally entitled to a minimum of 5.6 weeks of paid holiday per year — that is 28 days for someone working 5 days a week. Some employers offer more.

Your payslip may show the approximate cash value of your remaining leave. This is useful if your employment ends — in some cases you are entitled to be paid for untaken holiday.

What To Check Every Single Month

You do not need to spend an hour on this. Five things. Two minutes.

One — check your tax code. 1257L if you have one job and nothing unusual is going on.

Two — check your gross pay matches your contract.

Three — check your income tax looks proportionate to your salary band.

Four — check your NI deduction is at 8% on the relevant portion of your earnings.

Five — glance at your YTD figures and make sure they are tracking upward in a way that makes sense.

That is it. Consistent, simple, two minutes every payday.

What To Do If Something Looks Wrong

Call HMRC on 0300 200 3300.

They are actually helpful when you get through. Tell them your name, your NI number, and what you are querying. They can check your tax record, correct your code and in some cases process a refund on the spot.

If your employer’s payroll is the issue — HR or your payroll department is the first call. Keep records of everything in writing.

If you think you have overpaid tax across a full year, you can submit a claim through your HMRC personal tax account at gov.uk/personal-tax-account or by calling the number above.

One Last Thing

The UK tax system is not designed to be understood. It is designed to be paid.

But the people who take ten minutes to understand it keep more of their own money. Not because they are doing anything clever. Just because they know what to look for.

You know now.

Save this. Share it with someone who just started their first UK job and has never looked past the net pay figure.

This blog is for general information only. For advice specific to your personal tax situation, speak to a qualified accountant or tax adviser. Tax rules can change — always check the latest figures on gov.uk.